tidyfit is an R-package that facilitates

and automates linear and nonlinear regression and classification

modeling in a tidy environment. The package includes methods such as the

Lasso, PLS, time-varying parameter or Bayesian model averaging

regressions, and many more. The aim is threefold:

caret, the aim is not to cover a comprehensive set of

available packages, but rather a curated list of the most useful

ones.tidy data,

including verbs for regression and classification, automatic

consideration of grouped data, and tidy output formats

throughout.tidyfit builds on the tidymodels suite, but

emphasizes automated modeling with a focus on grouped data, model

comparisons, and high-volume analytics. The objective is to make model

fitting, cross validation and model output very simple and standardized

across all methods, with many necessary method-specific transformations

handled in the background.

tidyfit can be installed from CRAN or the development

version from GitHub

with:

# CRAN

install.packages("tidyfit")

# Dev version

# install.packages("devtools")

devtools::install_github("jpfitzinger/tidyfit")

library(tidyfit)tidyfit includes 3 deceptively simple functions:

regress()classify()m()All 3 of these functions return a tidyfit.models frame,

which is a data frame containing information about fitted regression and

classification models. regress and classify

perform regression and classification on tidy data. The functions ingest

a tibble, prepare input data for the models by splitting

groups, partitioning cross validation slices and handling any necessary

adjustments and transformations. The data is ultimately passed to the

model wrapper m() which fits the models.

To illustrate basic usage, suppose we would like to fit a financial factor regression for 10 industries with exponential weighting, comparing a WLS and a weighted LASSO regression:

progressr::handlers(global=TRUE)

tidyfit::Factor_Industry_Returns %>%

group_by(Industry) %>% # Ensures that a model is fitted for each industry

mutate(Weight = 0.96^seq(n(), 1)) %>% # Exponential weights

# 'regress' allows flexible standardized regression analysis in a single line of code

regress(

Return ~ ., # Uses normal formula syntax

m("lasso"), # LASSO regression wrapper, 'lambda' grid set to default

m("lm"), # OLS wrapper (can add as many wrappers as necessary here)

.cv = "initial_time_split", # Cross-validation method for optimal 'lambda' in LASSO

.mask = "Date", # 'Date' columns should be excluded

.weights = "Weight" # Specifies the weights column

) -> models_df

# Get coefficients frame

coef(models_df)The syntax is identical for classify.

m is a powerful wrapper for many different regression

and classification techniques that can be used with regress

and classify, or as a stand-alone function:

m(

<method>, # e.g. "lm" or "lasso"

formula, data, # not passed when used within regress or classify

... # Args passed to underlying method, e.g. to stats::lm for OLS regression

)An important feature of m() is that all arguments can be

passed as vectors, allowing generalized hyperparameter tuning or

scenario analysis for any method:

m("lasso", lambda = seq(0, 1, by = 0.1))m("robust", method = c("M", "MM"))m("subset", method = c("forward", "backward"))m("glm", family = list(binomial(link="logit"), binomial(link="probit")))Arguments that are meant to be vectors (e.g. weights) are recognized by the function and not interpreted as grids.

tidyfittidyfit currently implements the following methods:

| Method | Name | Package | Regression | Classification |

|---|---|---|---|---|

| Linear (generalized) regression or classification | ||||

| OLS | lm |

stats

|

yes | no |

| GLS | glm |

stats

|

yes | yes |

| Robust regression (e.g. Huber loss) | robust |

MASS

|

yes | no |

| Quantile regression | quantile |

quantreg

|

yes | no |

| ANOVA | anova |

stats

|

yes | yes |

| Regression or classification with L1 and L2 penalties | ||||

| LASSO | lasso |

glmnet

|

yes | yes |

| Ridge | ridge |

glmnet

|

yes | yes |

| Group LASSO | group_lasso |

gglasso

|

yes | yes |

| Adaptive LASSO | adalasso |

glmnet

|

yes | yes |

| ElasticNet | enet |

glmnet

|

yes | yes |

| Machine Learning | ||||

| Gradient boosting regression | boost |

mboost

|

yes | yes |

| Support vector machine | svm |

e1071

|

yes | yes |

| Random forest | rf |

randomForest

|

yes | yes |

| Quantile random forest | quantile_rf |

quantregForest

|

yes | yes |

| Neural Network | nnet |

nnet

|

yes | no |

| Factor regressions | ||||

| Principal components regression | pcr |

pls

|

yes | no |

| Partial least squares | plsr |

pls

|

yes | no |

| Hierarchical feature regression | hfr |

hfr

|

yes | no |

| Subset selection | ||||

| Best subset selection | subset |

bestglm

|

yes | yes |

| Genetic Algorithm | genetic |

gaselect

|

yes | no |

| General-to-specific | gets |

gets

|

yes | no |

| Bayesian regression | ||||

| Bayesian regression | bayes |

arm

|

yes | yes |

| Bayesian Ridge | bridge |

monomvn

|

yes | no |

| Bayesian Lasso | blasso |

monomvn

|

yes | no |

| Bayesian model averaging | bma |

BMS

|

yes | no |

| Bayesian Spike and Slab | spikeslab |

BoomSpikeSlab

|

yes | yes |

| Bayesian time-varying parameters regression | tvp |

shrinkTVP

|

yes | no |

| Mixed-effects modeling | ||||

| Generalized mixed-effects regression | glmm |

lme4

|

yes | yes |

| Specialized time series methods | ||||

| Markov-switching regression | mslm |

MSwM

|

yes | no |

| Feature selection | ||||

| Pearson correlation | cor |

stats

|

no | no |

| Chi-squared test | chisq |

stats

|

yes | yes |

| Minimum redundancy, maximum relevance | mrmr |

mRMRe

|

yes | yes |

| ReliefF | relief |

CORElearn

|

yes | yes |

See ?m for additional information.

It is important to note that the above list is not complete, since

some of the methods encompass multiple algorithms. For instance,

“subset” can be used to perform forward, backward or exhaustive search

selection using leaps. Similarly, “lasso” includes certain

grouped LASSO implementations that can be fitted with

glmnet.

In this section, a minimal workflow is used to demonstrate how the package works. For more detailed guides of specialized topics, or simply for further reading, follow these links:

tidyfit includes a data set of financial Fama-French

factor returns freely available here.

The data set includes monthly industry returns for 10 industries, as

well as monthly factor returns for 5 factors:

data <- tidyfit::Factor_Industry_Returns

# Calculate excess return

data <- data %>%

mutate(Return = Return - RF) %>%

select(-RF)

data

#> # A tibble: 7,080 × 8

#> Date Industry Return `Mkt-RF` SMB HML RMW CMA

#> <dbl> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 196307 NoDur -0.76 -0.39 -0.44 -0.89 0.68 -1.23

#> 2 196308 NoDur 4.64 5.07 -0.75 1.68 0.36 -0.34

#> 3 196309 NoDur -1.96 -1.57 -0.55 0.08 -0.71 0.29

#> 4 196310 NoDur 2.36 2.53 -1.37 -0.14 2.8 -2.02

#> 5 196311 NoDur -1.4 -0.85 -0.89 1.81 -0.51 2.31

#> 6 196312 NoDur 2.52 1.83 -2.07 -0.08 0.03 -0.04

#> 7 196401 NoDur 0.49 2.24 0.11 1.47 0.17 1.51

#> 8 196402 NoDur 1.61 1.54 0.3 2.74 -0.05 0.9

#> 9 196403 NoDur 2.77 1.41 1.36 3.36 -2.21 3.19

#> 10 196404 NoDur -0.77 0.1 -1.59 -0.58 -1.27 -1.04

#> # ℹ 7,070 more rowsWe will only use a subset of the data to keep things simple:

df_train <- data %>%

filter(Date > 201800 & Date < 202000)

df_test <- data %>%

filter(Date >= 202000)Before beginning with the estimation, we can activate the progress

bar visualization. This allows us to gauge estimation progress along the

way. tidyfit uses the progressr-package

internally to generate a progress bar — run

progressr::handlers(global=TRUE) to activate progress bars

in your environment.

For purposes of this demonstration, the objective will be to fit an

ElasticNet regression for each industry group, and compare results to a

robust least squares regression. This can be done with

regress after grouping the data. For grouped data, the

functions regress and classify estimate models

for each group independently:

model_frame <- df_train %>%

group_by(Industry) %>%

regress(Return ~ .,

m("enet"),

m("robust", method = "MM", psi = MASS::psi.huber),

.cv = "initial_time_split", .mask = "Date")Note that the penalty and mixing parameters are chosen automatically

using a time series train/test split

(rsample::initial_time_split), with a hyperparameter grid

set by the package dials. See ?regress for

additional CV methods. A custom grid can easily be passed using

lambda = c(...) and/or alpha = c(...) in the

m("enet") wrapper.

The resulting tidyfit.models frame consists of 3

components:

Industry column, the model name, and grid ID (the ID for

the model settings used).estimator_fct, size (MB) and

model_object columns. These columns contain information on

the model itself. The model_object is the fitted

tidyFit model (an R6 class that contains the

model object as well as any additional information needed to perform

predictions or access coefficients)settings, as well as (if applicable)

messages and warnings.subset_mod_frame <- model_frame %>%

filter(Industry %in% unique(Industry)[1:2])

subset_mod_frame

#> # A tibble: 4 × 8

#> Industry model estimator_fct `size (MB)` grid_id model_object settings

#> <chr> <chr> <chr> <dbl> <chr> <list> <list>

#> 1 Enrgy enet glmnet::glmnet 1.21 #001|100 <tidyFit> <tibble>

#> 2 Shops enet glmnet::glmnet 1.21 #001|049 <tidyFit> <tibble>

#> 3 Enrgy robust MASS::rlm 0.0638 #0010000 <tidyFit> <tibble>

#> 4 Shops robust MASS::rlm 0.0638 #0010000 <tidyFit> <tibble>

#> # ℹ 1 more variable: warnings <chr>Let’s unnest the settings columns:

subset_mod_frame %>%

tidyr::unnest(settings, keep_empty = TRUE)

#> # A tibble: 4 × 13

#> Industry model estimator_fct `size (MB)` grid_id model_object alpha weights

#> <chr> <chr> <chr> <dbl> <chr> <list> <dbl> <list>

#> 1 Enrgy enet glmnet::glmnet 1.21 #001|100 <tidyFit> 0 <NULL>

#> 2 Shops enet glmnet::glmnet 1.21 #001|049 <tidyFit> 0 <NULL>

#> 3 Enrgy robust MASS::rlm 0.0638 #0010000 <tidyFit> NA <NULL>

#> 4 Shops robust MASS::rlm 0.0638 #0010000 <tidyFit> NA <NULL>

#> # ℹ 5 more variables: family <chr>, lambda <dbl>, method <chr>, psi <list>,

#> # warnings <chr>The tidyfit.models frame can be used to access

additional information. Specifically, we can do 4 things:

The fitted tidyFit models are stored as an

R6 class in the model_object column and can be

addressed directly with generics such as coef or

summary. The underlying object (e.g. an lm

class fitted model) is given in ...$object (see here

for another example):

subset_mod_frame %>%

mutate(fitted_model = map(model_object, ~.$object))

#> # A tibble: 4 × 9

#> Industry model estimator_fct `size (MB)` grid_id model_object settings

#> <chr> <chr> <chr> <dbl> <chr> <list> <list>

#> 1 Enrgy enet glmnet::glmnet 1.21 #001|100 <tidyFit> <tibble>

#> 2 Shops enet glmnet::glmnet 1.21 #001|049 <tidyFit> <tibble>

#> 3 Enrgy robust MASS::rlm 0.0638 #0010000 <tidyFit> <tibble>

#> 4 Shops robust MASS::rlm 0.0638 #0010000 <tidyFit> <tibble>

#> # ℹ 2 more variables: warnings <chr>, fitted_model <list>To predict, we need data with the same columns as

the input data and simply use the generic predict function.

Groups are respected and if the response variable is in the data, it is

included as a truth column in the resulting object:

predict(subset_mod_frame, data)

#> # A tibble: 2,832 × 4

#> # Groups: Industry, model [4]

#> Industry model prediction truth

#> <chr> <chr> <dbl> <dbl>

#> 1 Enrgy enet -3.77 2.02

#> 2 Enrgy enet 3.90 3.69

#> 3 Enrgy enet -2.40 -3.91

#> 4 Enrgy enet -3.30 -0.61

#> 5 Enrgy enet 0.762 -1.43

#> 6 Enrgy enet -0.293 4.36

#> 7 Enrgy enet 3.68 4.54

#> 8 Enrgy enet 2.31 0.8

#> 9 Enrgy enet 7.26 1.09

#> 10 Enrgy enet -2.53 3.74

#> # ℹ 2,822 more rowsFinally, we can obtain a tidy frame of the

coefficients using the generic coef function:

estimates <- coef(subset_mod_frame)

estimates

#> # A tibble: 24 × 5

#> # Groups: Industry, model [4]

#> Industry model term estimate model_info

#> <chr> <chr> <chr> <dbl> <list>

#> 1 Enrgy enet (Intercept) -0.955 <tibble [1 × 4]>

#> 2 Enrgy enet Mkt-RF 1.20 <tibble [1 × 4]>

#> 3 Enrgy enet SMB 0.703 <tibble [1 × 4]>

#> 4 Enrgy enet HML -0.00208 <tibble [1 × 4]>

#> 5 Enrgy enet RMW -0.622 <tibble [1 × 4]>

#> 6 Enrgy enet CMA 1.32 <tibble [1 × 4]>

#> 7 Shops enet (Intercept) 1.03 <tibble [1 × 4]>

#> 8 Shops enet Mkt-RF 0.0849 <tibble [1 × 4]>

#> 9 Shops enet SMB 0.0353 <tibble [1 × 4]>

#> 10 Shops enet HML -0.0149 <tibble [1 × 4]>

#> # ℹ 14 more rowsThe estimates contain additional method-specific information that is

nested in model_info. This can include standard errors,

t-values and similar information:

tidyr::unnest(estimates, model_info)

#> # A tibble: 24 × 8

#> # Groups: Industry, model [4]

#> Industry model term estimate lambda dev.ratio std.error statistic

#> <chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 Enrgy enet (Intercept) -0.955 0.536 0.812 NA NA

#> 2 Enrgy enet Mkt-RF 1.20 0.536 0.812 NA NA

#> 3 Enrgy enet SMB 0.703 0.536 0.812 NA NA

#> 4 Enrgy enet HML -0.00208 0.536 0.812 NA NA

#> 5 Enrgy enet RMW -0.622 0.536 0.812 NA NA

#> 6 Enrgy enet CMA 1.32 0.536 0.812 NA NA

#> 7 Shops enet (Intercept) 1.03 50.1 0.173 NA NA

#> 8 Shops enet Mkt-RF 0.0849 50.1 0.173 NA NA

#> 9 Shops enet SMB 0.0353 50.1 0.173 NA NA

#> 10 Shops enet HML -0.0149 50.1 0.173 NA NA

#> # ℹ 14 more rowsAdditional generics such as fitted or resid

can be used to obtain more information on the models.

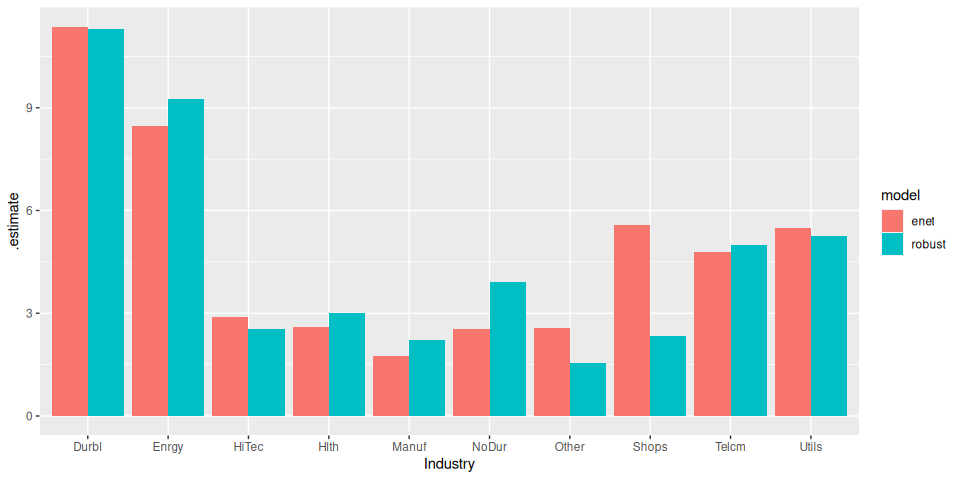

Suppose we would like to evaluate the relative performance of the two

methods. This becomes exceedingly simple using the

yardstick package:

model_frame %>%

# Generate predictions

predict(df_test) %>%

# Calculate RMSE

yardstick::rmse(truth, prediction) %>%

# Plot

ggplot(aes(Industry, .estimate)) +

geom_col(aes(fill = model), position = position_dodge())

The ElasticNet performs a little better (unsurprising really, given the small data set).

A more detailed regression analysis of Boston house price data using a panel of regularized regression estimators can be found here.